Insurance Compass Switzerland 2026

The Swiss Insurance Association (SIA) is launching an annual quantitative overview of the Swiss private insurance industry. The new publication, Insurance Compass Switzerland, presents key metrics, analyses structural trends and shows that insurers are a major source of stability for the economy and society – as risk bearers, investors, employers and providers of long-term security.

When people talk about insurance, they tend to talk about premiums. The focus is rarely on the economic contributions that underlie insurance cover: the amount of risk that insurers bear, how much capital they invest, the number of jobs they create or how much they contribute to the stability of the economy and society. This is precisely what the Swiss Insurance Association (SIA) aims to show every year going forward with its new publication, Insurance Compass Switzerland.

The new publication provides an overview of key metrics, trends and structural developments in the Swiss private insurance industry. It combines quantitative data with qualitative classification and highlights the role insurers play in the economic system – in the daily lives of policyholders, as part of the financial centre and as long-term investors.

Insurance Compass is aimed at decision-makers in business, politics and the public sector. Its goal is to provide an up-to-date, clear, reliable overview of the industry. The publication is based on publicly available statistics, regulatory data and the SIA’s own calculations.

Insurers as a source of economic stability

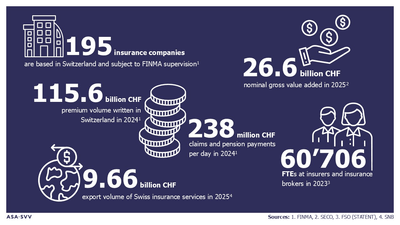

Insurance Compass highlights the scope and importance of the insurance industry. There are 195 insurance companies based in Switzerland and supervised by FINMA. In 2025, they generated nominal gross value added of CHF 26.6 billion. Including insurance-related activities, value added amounted to CHF 31.4 billion in 2024.

Viewed from a long-term perspective, insurance companies grow faster in real terms than the economy as a whole. The average annual growth rate of gross value added for insurers in the period from 2005 to 2024 was 3.1 per cent, higher than the 2.0 per cent for gross domestic product. This development was driven in particular by property and accident insurance and insurance-related activities.

The industry is also an important employer, with insurance companies accounting for more than 44,000 full-time positions. At the same time, the insurance industry is one of the most productive in Switzerland. Despite having a relatively small workforce, it makes a disproportionately large contribution to economic output; with around CHF 500,000 in value added per full-time equivalent, the industry boasts a labour productivity rate 2.6 times higher than the overall economic average.

CHF 238 million a day in claims and pensions

The value of insurance becomes particularly apparent where risks have a tangible financial impact, for example after an accident, in cases of illness, following a natural disaster or in the event of a liability claim or death. In 2024, private insurers paid out an average of CHF 238 million a day in claims and pensions.

These benefits do more than just provide stability for individual households and businesses – they also safeguard economic value chains and help ensure that risks to the economy and society remain manageable.

Taking a long-term view with CHF 526 billion in investments

Insurers not only assume risks; they also pump capital into the economy. In 2024, Swiss private insurers invested CHF 526 billion in the capital market. Their investments are geared towards the long term and are intended to ensure they can meet their obligations to their policyholders.

This makes insurers important institutional investors. They provide capital for governments, companies, real estate, infrastructure and other long-term financing initiatives, always on the condition that security, risk-bearing capacity and return remain balanced in the interests of their policyholders.

Varying dynamics in the segments

Insurance Compass also makes it clear that the insurance industry is anything but homogeneous. There are various segments within the industry, and they all have their own challenges to deal with.

Development in non-life insurance is dominated by rising construction, repair and healthcare costs and natural hazards. For 2025, the SIA expects premium volume growth of 3.0 per cent in non-life business, while property insurance is experiencing particularly strong growth of 4.4 per cent.

We are seeing structural shifts in life insurance. While individual life is growing, group life remains under pressure due to demographic developments, capital market conditions and regulatory requirements. Nevertheless, life insurers remain a key element of the second and third pillars.

Meanwhile, reinsurance underscores Switzerland’s standing on the international stage as a business location. Reinsurers take on substantial risks, diversify them globally and create additional capacity for primary insurers, companies and governments. Reinsurance accounted for around 78 per cent of Swiss exports in terms of insurance services in 2024.

Insurability needs a sound operating framework

Insurance Compass shows a common thread running through all divisions, namely that insurability does not just happen on its own. It needs solid capitalisation, risk-adjusted premiums, effective prevention, functioning markets and a reliable operating framework.

Swiss insurers are in a good position in terms of capitalisation. The average solvency ratio stood at 246 per cent at the beginning of 2025, well above the regulatory minimum requirement. At the same time, regulatory complexity is increasing. A balance between effective protection, proportionality and international connectivity remains crucial.

With Insurance Compass, the SIA is creating a new basis for dialogue about the role of the insurance industry – and about the prerequisites for ensuring that insurance cover remains widely available, viable and innovative in the future.

Insurance Compass Switzerland

Insurance Compass Switzerland is an annual publication issued by the Swiss Insurance Association (SIA) on the economic importance and development of the Swiss private insurance industry. It compiles key metrics, analyses structural developments and highlights the role insurers play as risk bearers, employers, investors and sources of stability for the economy and society.

The publication is based on publicly available statistics, regulatory data and the SIA’s own calculations and analyses. The most important sources include FINMA, the Federal Statistical Office (FSO), the State Secretariat for Economic Affairs (SECO), the Swiss National Bank (SNB) and BAK Economics.

The first edition of Insurance Compass Switzerland was published in June 2026. It features an overview of the Swiss insurance market and separate chapters on non-life insurance, life insurance and reinsurance.

Download

You may also be interested

- Key financial figures | 5 February 2026

Premium volumes in the Swiss insurance sector

In 2025, Swiss private insurers’ premium volumes once again experienced pleasing growth, according to data from the Swiss Insurance Association (SIA).

- Key financial figures | 4 September 2025

The Swiss insurance market: companies and market shares

The insurance market is highly competitive. 2024 saw roughly 195 private insurers compete for the favour of policyholders across five insurance branches.

- Key financial figures | 4 September 2025

Balance sheet and income statement for the 2024 insurance market

FINMA compiles data on business development within the insurance companies that fall under its supervision and provides an overview of industry key figures in the Insurance Market Report.