Personal accountability as a success factor for major risks and retirement provision

In 2023, Swiss private insurers’ premium volume once again experienced pleasing growth, according to projections by the Swiss Insurance Association SIA. This sees the private insurance industry live up to its reputation as a stabilising force for the Swiss economy. In addition, the association emphasises the strength of private-sector retirement solutions – whether in hedging major risks or in retirement provision. The foundations of this latter area are to be shored up in the near term.

Switzerland’s private insurers can once again report pleasing growth at their annual press conference, thereby living up to their reputation as a stabilising force for the Swiss economy. However, they do not want to rest on their laurels. Trends relating to the overarching conditions in Switzerland, in particular, are being scrutinised. ‘We feel a certain sense of personal accountability as an industry association – and this is growing in the current political climate,’ points out Stefan Mäder, chairman of the insurance association. He believes that the overarching conditions of the Swiss economy, which are linked to economic freedom and personal accountability, are increasingly coming under pressure: ‘The call for greater state involvement damages Switzerland’s ability to innovate and, by extension, harms our economy and our country’s prosperity in the long term.’ He also believes that this would impact the insurance industry’s scope for development.

Sector as an example of well-functioning personal accountability

The association serves as a reminder that the insurance industry is a good example of how personal accountability can function well on a societal level. After all, it has organised solidarity-based communities, situated within the market economy, to protect against risk since its earliest days. For Juan Beer, SIA vice-president and CEO of Zurich Schweiz, there is no reason to call this principle into question: ‘The insurance industry can offer efficient, effective solutions. Systems organised exclusively by the state should only be considered if there are no other options available in the private sector.’ Beer illustrates this not least with reference to the risk of earthquakes. Although the risk is globally insurable, Switzerland’s parliament is, in his eyes, adding a state-backed solution in the form of contingent liability. In his view, this merely gives the illusion of a solution: Especially for SMEs the contingent liability is incomplete, functions as an additional tax and would make the crisis worse if disaster were to strike.

In the field of retirement provision, the association also warns against overweighting state OASI. The SIA is an advocate of the tried-and-trusted three-pillar system with its current weighting. It is important not to buy into false promises: ‘The goal cannot be to take a scattergun approach to building up benefits. Instead, we need efforts to stabilise retirement provision in the long run. For these reasons, the SIA rejects the popular initiative in favour of a 13th AHV pension,’ emphasises Stefan Mäder as he looks towards the upcoming referenda on 3 March 2024.

Growth in all branches of non-life business

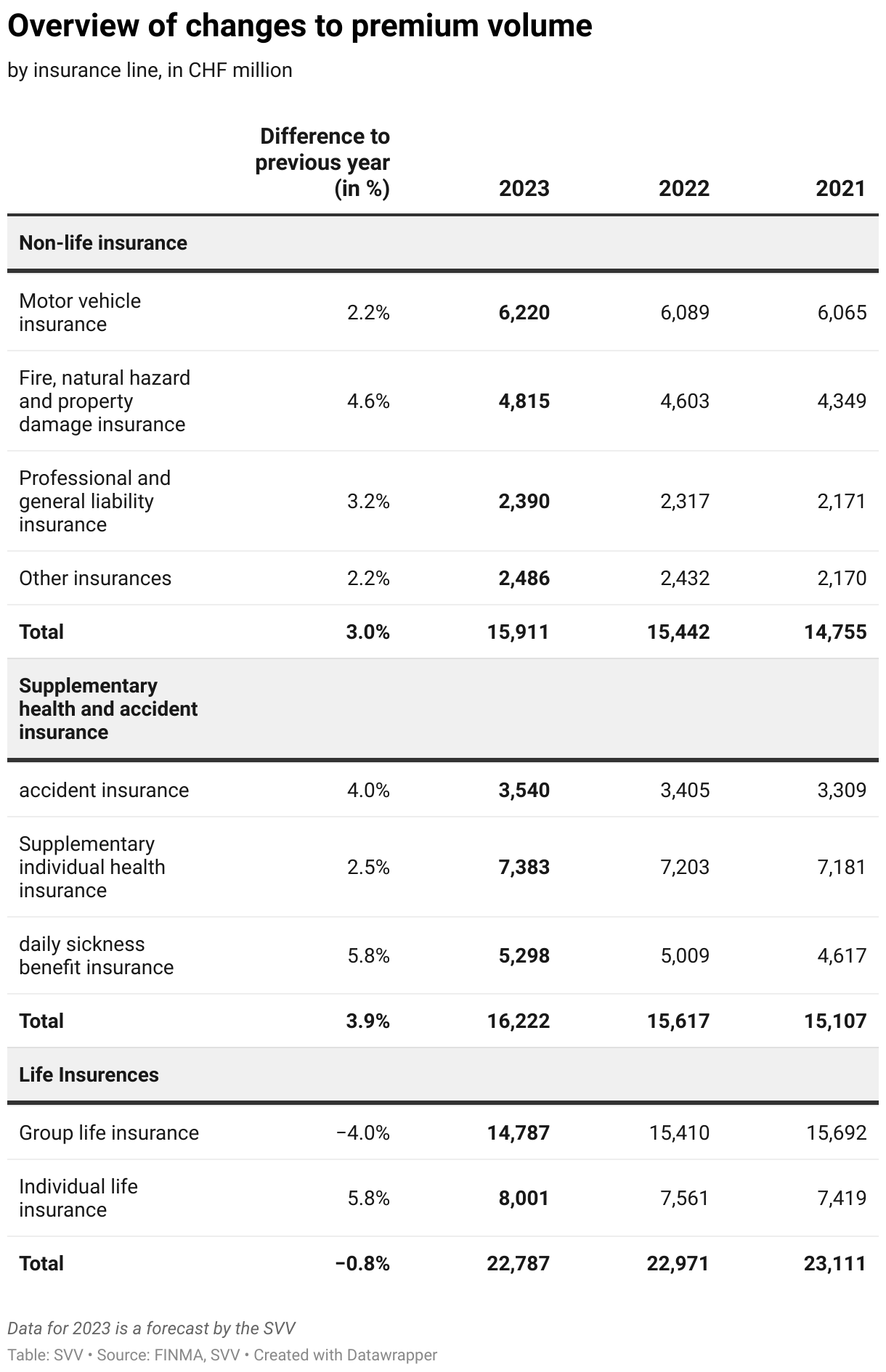

Nevertheless, the private insurance industry can look back on a successful 2023, with premiums growing by around three per cent in the non-life business. ‘This trend is not just due to ongoing cost increases in the past year, but also robust societal demand,’ said Urs Arbter, association director, commenting on the development. While the growth in liability and property insurance is largely due to higher repair costs and the appreciation of the goods insured, wage growth and, not least, new insurance products – such as cyber insurance – led to a higher premium volume.

Supplementary health insurance also experienced a slight uptick in portfolio size: Premium volume grew by 2.5 per cent while premiums themselves only increased slightly. The picture is rather different for the field of daily sickness benefits, which expanded by 5.8 per cent. This was primarily caused by wage increases and the fact that premiums needed to be adjusted upwards following higher benefit payments.

Note to editors

The Swiss Insurance Association (SIA) represents the interests of the private insurance industry at national and international level. It has approximately 70 members, which include global primary insurers and reinsurers, as well as many nationally oriented specialist non-life, life and supplementary health insurers. The sector is one of the most productive and highest value-added sectors of the economy. The private insurance sector employs about 50,000 people in Switzerland. With its expertise in risk coverage and hazard prevention, it assumes economic responsibility. Private insurers make a key contribution to the stability of the economic system and prosperity within Switzerland. As a result, the SIA is committed to the sustainable development of the industry and its locations.

Media contact

Swiss Insurance Association SIA

Thilo Kleine, Spokesperson

Telefon: +41 44 208 28 14

E-Mail: media svv [dot] ch

svv [dot] ch